The Banking Act of 1934 made Swiss banking secret unique by rendering any persons betraying it criminals.

In short, it put Swiss bankers in the same category with doctors and lawyers who are all bound by law to keep their clients’ secrets… well, secret.

I could tell you all about the minimum $100,000 bank deposits. Because if you are a foreign national, that’s the absolute minimum allowing you to open a savings account in Confoederatio Helvetica (CH).

Or I could tell you about the famous numbered accounts, which do not require any identification to access, except for a special account number.

But I guess the most singular characteristic of Swiss bank accounts is the secrecy surrounding them.

People say that that’s a bad thing but I disagree.

Private wealth is best kept in private hands. The state should not be able to dispossess private citizens of their savings.

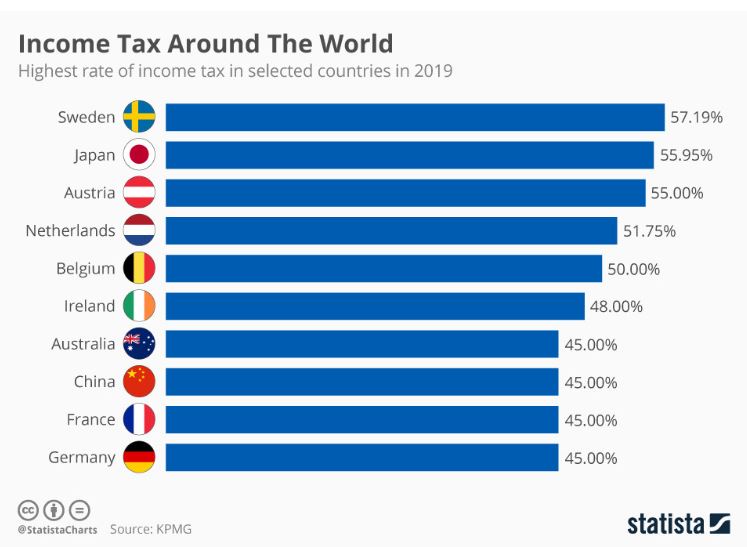

The Swiss believe in this principle. The rest of the world does not. That is why each and every of the 26 cantons of the Swiss Confederation has a different tax rate.

These oscillate ever so often making the lives of smart foreigners of discerning means easier when it comes to selecting a canton for their residence. Some cantons are even known for offering a one time tax deal to a foreign investor or depositor of substantive means.

Say you have $10 Million and you go to canton Zug. You meet with the cantonal tax assessor and negotiate a percentage (7–10%) that you will only pay once. The other $9 million you are free to deposit in a Swiss bank account, without having to worry about taxation.

Even those working in Switzerland are better off than most income earners around the globe. Earning one’s living is encouraged by the taxman. Starting a family even more so; the bigger the family gets, the less one pays in taxes.

If we compare the flat tax rates that foreign investors get from Swiss tax authorities with the level of taxation prominent in the vast majority of the developed world, we get a sense of the level of downright theft perpetrated by the taxman almost everywhere else.

The Swiss encourage saving at all levels of society, by their own citizens but also by rich foreigners. The two big levers, bank secrecy and reasonable taxation make sure that people continue to save, instead of spending, and that they pay their fair share instead of evading or avoiding taxation.

So year after year, deposits grow and people prosper. But what to do with all that cash surplus? Tricky question, eh!

Personally, I’d invest in gold. The world is in turmoil. Politics is becoming a freak show. Fiat currency is only as good as the people’s trust in it. Paper money is only good for day to day transactions. Saving requires gold. But this is another discussion altogether.

However, if you open up a business in CH, be prepared to pay income tax, revenue tax, dividend tax, etc, etc.

But if you come to Switzerland as a tourist/resident/bank depositor or direct investor, the one time taxation deal applies to the volume of the funds you brought in. The Swiss are very serious about people’s money and they think over the long term.

And that, my friends, is why smart people of discerning means do their banking in CH.

Because it is safe, private, and cheap.